The world of commerce is no more linear. Today businesses are aiming to provide an integrated and multi-dimensional experience to all the stakeholders. This integrated and multidimensional experience, or the “Omni-Channel” experience is a result of consumer’s access to multiple channels of commerce and payment methods. Powered by digital innovations, democratization of technology, and lower costs, the demand for a seamless omni-channel experience has grown massively in the recent times.

Modern day merchants and businesses have been the biggest drivers of these omni-channel experiences but efficient merchant management solutions by top acquiring institutions are the pillars which help architect these experiences. An efficient merchant management system is the backbone over which modern merchant acquiring businesses are standing and growing. While there are multiple factors that determine the efficiency of a merchant management system, certain elements remain critical across all business environments and determine the success of the business and the solution.

Seven factors that help architect a modern-day omnichannel experience:

-

- Ease of Onboarding and Maintenance: An acquirer bank deals with multiple types of merchants, businesses varying in size, scale, mode of operations and physical & digital footprint. But the bank cannot have a separate onboarding and setup process for all. A smooth onboarding process catering to all businesses helps banks manage their entire merchant portfolio though a single integrated system. Features like merchant ID generation, ease of merchant navigation, and auto fee plan generation significantly improves the bank’s ability to setup, manage, and grow their merchant business.

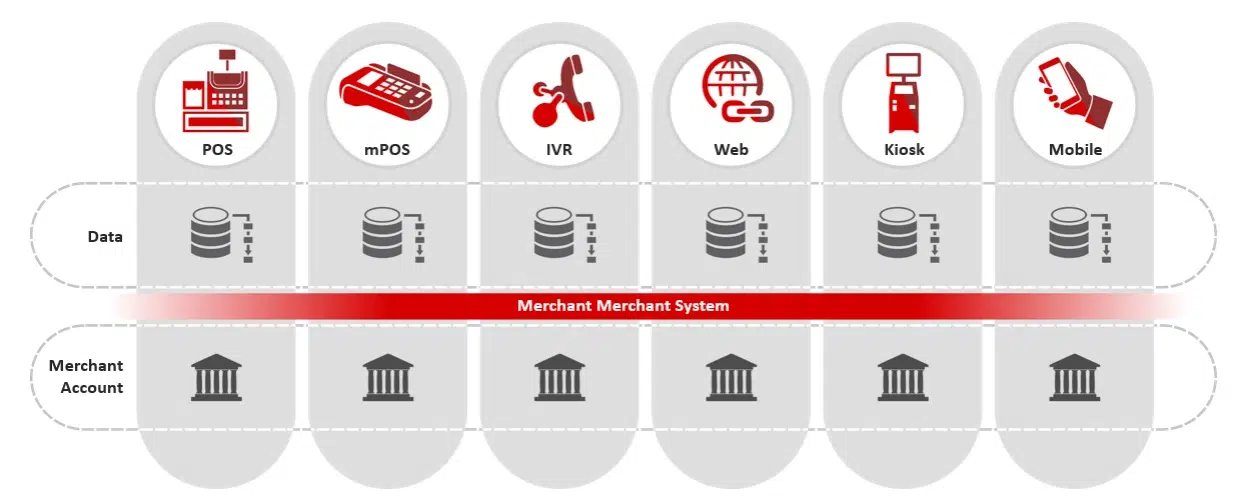

- Number of Delivery Channels & Payment Methods: The customer today is spoilt with choices. Be it the choice to pay in-store in a card present environment via a POS terminal or making a digital payment using an integrated payment gateway, or other channels like IVR, Kiosks, and more; used to make payments via multiple methods – OTP, Card, UPI, QR, Email, SMS – the merchant management system should have the capability to support all major payments transactions, capture data across channels, consolidate and manage settlements and disputes.

- Number of Integrations: Banks and acquirers are moving towards a modular, API based, simpler user interfaces and other external integrations with different systems that allow banks to synchronize and manage merchant data both in an online as well as offline setup. Today, an efficient merchant management system should be able to provide the compatibility to integrate with multiple systems, across businesses and technology environments.

- Customization and Flexibilities: Personalization is a common theme across businesses. Providing customization at an acquirer level, or an aggregator level, or a merchant level, and flexibility to determine the number, type and rate of fees charged depending on the nature and size of business helps banks deliver higher value to its customers and at the same time reduce the business risk. Acquirers should be able set up a billing structure tailored to a merchant’s business needs. A modern merchant management system allows different merchant entities within the hierarchy to be tied to a specific fee structure.

- Ease of Settlement and Dispute Management: An integrated merchant management system can easily automate the settlement and dispute management workflows by providing the flexibility to configure multiple settlement cycles in a day, supporting multiple file formats, and currencies within the same system. Following a pre-determined workflow for Merchant and Interchange Settlement reduces the TAT, as well as the dispute instances significantly, which improves the overall efficiency of the business function.

- Efficient Reporting and Visibility: Visibility and Reporting via interactive dashboards and portals at multiple levels, i.e., at the bank level, aggregator level and the merchant level provides different insights to all stakeholders. Real time insights into business through multiple reports improves the business’ capability to look at acquiring operations through analytical lens across multiple parameters. Such insights eventually help the acquirer make better business decisions, adds agility in workflows and helps reduce business leakages.

- Secure Fraud and Risk Management: Payment businesses are built on trust. Trust that the transactions are not only made in a secure, risk-free environment but the data and access is also maintained in a secure environment. Following hygiene checks like PA DSS 3.2 compliances, efficient merchant and transaction risk categorizations, dynamic risk checks help boost the merchant and acquirer confidence on the merchant management system.

Apart from the above mentioned 7 factors, additional factors like an efficient merchant portal, centralized repositories, multiple capture modes, and multilingual support adds on to the overall efficiency of a modern day merchant management system.

FSS’ Acquiring Suite has been powering banks and financial institutions for more than 30 years. FSS’ Merchant Hub is a modern-day offering catering to the core needs of acquiring banks and merchants and provide a complete solution catering to a bank’s technology needs.

To know more, write to us at products@fsstech.com